KLIA at 14%: Dubai's Playbook, Changi's Counter-Model

Two regional hubs lived this growth curve before. Their playbooks diverged. Malaysia's choice begins now.

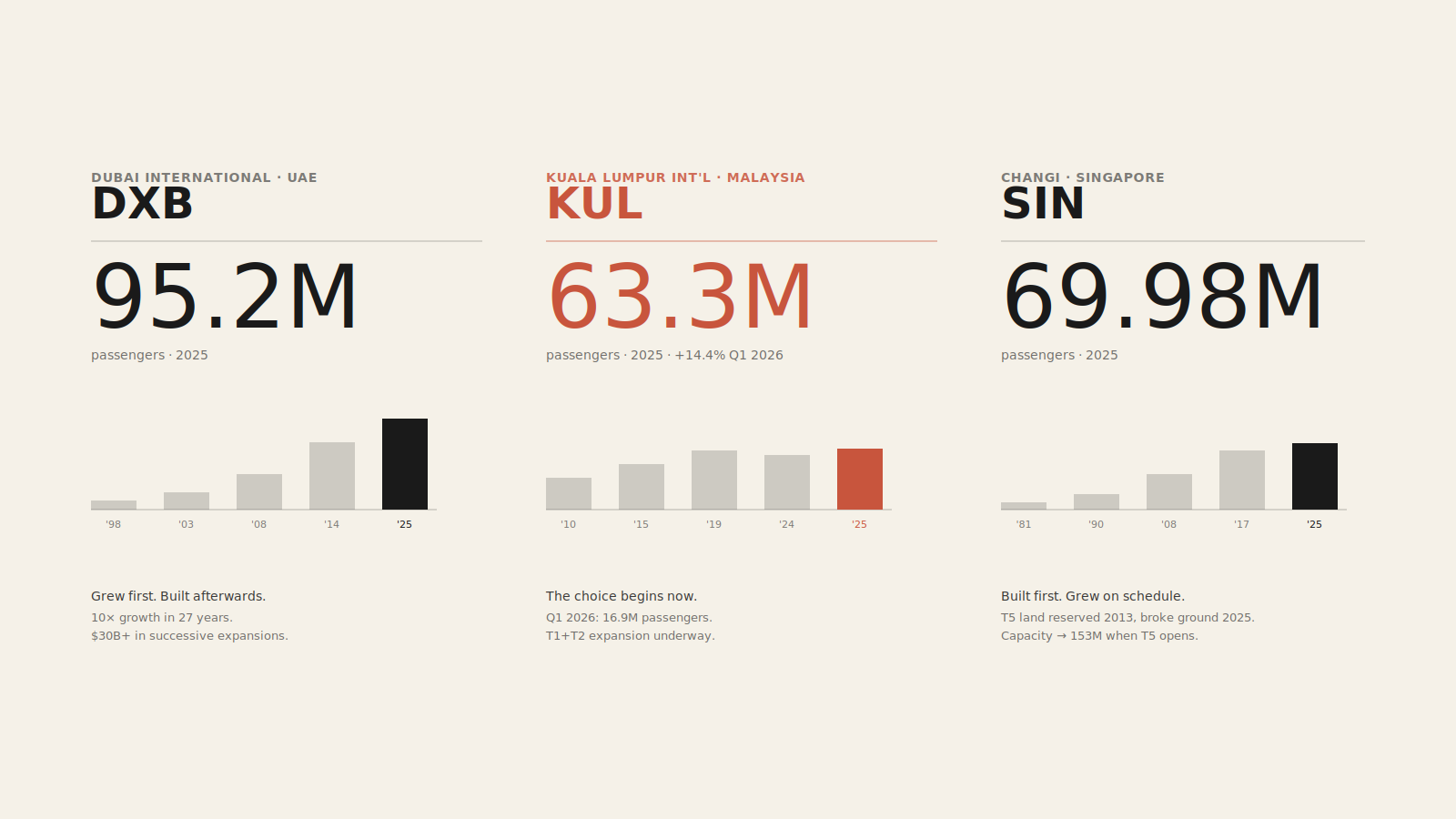

The brief - KLIA handled 16.9 million passengers in Q1 2026, up 14.4% year-on-year. The growth curve mirrors what Dubai International lived through between 2003 and 2014. Two regional hubs have lived this moment before. Their playbooks diverged. What Malaysia chooses next will define hub status for the decade ahead.

Malaysia Airports Holdings Bhd (MAHB) announced on 27 April that Kuala Lumpur International Airport (KLIA) handled 16.9 million passenger movements in Q1 2026 — a 14.4% increase year-on-year. The Hari Raya Aidilfitri period alone saw more than 3.1 million passengers pass through the terminals. Managing director Mohd Izani Ghani framed the priority as “matching this momentum with the right capacity, seamless operations and targeted improvements on the ground.”

This is the right priority. It is also exactly what Dubai International Airport (DXB) was saying in 2003, when it had just doubled capacity from 10 to 23 million. What happened next at DXB became over $30 billion in cumulative aviation infrastructure investment. It is worth looking at.

The trajectory looks familiar

KLIA handled 57.08 million passengers in 2024, placing it among the world’s top 30 airports. It closed 2025 at 63.3 million, a 10.8% year-on-year increase. With Q1 2026 already at 16.9 million and Visit Malaysia 2026 expected to support demand, the airport could plausibly land around 68–72 million by year-end if momentum holds.

MAHB and the Ministry of Transport have publicly outlined an expansion plan: Terminal 1 capacity is to rise from 30 to 59 million passengers per annum, Terminal 2 from 45 to 67 mppa, with a fourth runway and a Terminal 3 also under consideration. Short-term measures are already in motion — additional autogates, self-check-in kiosks, a Hajj and Umrah terminal in planning.

That growth curve is not new. It mirrors what DXB lived through between 2003 and 2014.

Two regional mirrors, two operational models

The DXB mirror. Dubai handled 9.7 million passengers in 1998. By 2003: 18 million. By 2014: 70.4 million, becoming the world’s busiest international hub. By 2025: 95.2 million. The model was unambiguous — grow first, expand infrastructure to catch up. Operational cost: three successive extensions (Terminal 3 in 2008, Concourse A in 2013, Concourse D in 2016) to chase demand. Each expansion uncovered new chokepoints that were invisible before. As Dubai Airports CEO Paul Griffiths put it earlier this year, reflecting on a decade of sustained record traffic: “Airports are often defined by moments of intensity, but long-term performance is defined by how well those moments are sustained.”

The Changi counter-model. Singapore opened Terminal 1 in 1981, Terminal 2 in 1990, Terminal 3 in 2008, Terminal 4 in 2017. Terminal 5 was announced in 2013, the land reserved, construction broke ground in May 2025 — for a delivery in the mid-2030s. That’s 17+ years between announcement and operational opening. Current capacity sits at 90 million passengers across four terminals. Total capacity will reach 153 million once T5 comes online. The logic is inverted: structured phasing across decades, vertical integration through Changi Airport Group, full Terminal 2 refurbishment during the pandemic as a pre-emptive investment ahead of the recovery.

KLIA in 2026 sits in a position editorially comparable to DXB in 2003: a hub with strong momentum, ambitious capacity plans on paper, and the operational test still ahead.

Four observations from regional precedents

Past experiences are not a forecast — context, governance and capital structures differ between hubs. But the regional record offers four operational signals worth tracking.

Physical capacity is not operational capacity. DXB’s experience suggests that even successive infrastructure deliveries can leave new bottlenecks visible only at higher volumes — security throughput, baggage handling, ground turnaround. Targeting 100M passengers says less than the SLA the airport actually sustains at that volume. The metric to watch is not capacity built, but service level held under peak.

Operational governance tends to precede growth, not follow it. DXB structured what is often referred to as a “oneDXB” model — an airport-wide community forum coordinating 100+ stakeholders (airlines, ground handlers, security, immigration, retail concessions). Changi operates under a fully integrated Airport Group from origin. Whether and how MAHB structures an equivalent governance layer at scale is one of the variables to watch.

The second airport horizon matters. Dubai started building DWC in 2010 with a $35 billion target, ultimate capacity 260 million. Changi reserved land for T5 in 2013, broke ground twelve years later. KLIA’s current public roadmap — expanded T1, expanded T2, a possible T3 and fourth runway — does not yet include a comparable second-hub or far-horizon timeline. That may evolve.

The narrative tends to shift from “fastest growing” to “most resilient.” This is the deeper signal. Both DXB and Changi have moved past the “we are growing fast” story. Their public messaging now centres on sustained performance rather than peak volume. Long-term hub status appears to be built on the consistency of the SLA across years, not the height of the quarterly statistic.

The real question for the next 18 months

KLIA today sits in a position editorially comparable to DXB in 2003, with the Changi model nearby as a reminder that a different path was possible. Both playbooks are publicly available. The question is not whether growth arrives — it is here. The question is which mix of operational choices MAHB makes, and on what timeline.

Five years from now, the operational SLA will tell more than the quarterly traffic statistics.

Subscribe to receive new briefs and long reads on operational realities across ASEAN and the GCC.